[share_sc]

If you are dealing with a combination of debt types such as medical debt, payday loans, and credit card debt, you may be considering debt consolidation.

In short, debt consolidation is where you are consolidating multiple debts that have payments associated with one debt and one single monthly payment. You can consolidate debt that has a monthly payment or one lump sum payment.

As someone who worked as an executive at a debt consolidation company for many years, I tend to think that I have a more insider, exclusive via of the pros and cons of debt consolidation.

Two types of Debt Consolidation

Before jumping into the advantages and disadvantages of debt consolidation, it’s important to understand that there are two types of debt consolidation:

- Debt consolidation loans

- Debt consolidation programs.

These are vastly different, but it’s important to understand the differences because some deceptive companies may attempt to say, “you don’t qualify for a debt consolidation loan, but you qualify for a debt consolidation program”. A debt consolidation program is where you would enter your debts into a program, let the accounts go past due, and then the program would try to settle the debts. You can be sued in a debt consolidation program because your debt goes behind and your credit score will be negatively affected.

We will cover debt consolidation loan pros and cons in this article, but I plan to write another article covering a debt consolidation program

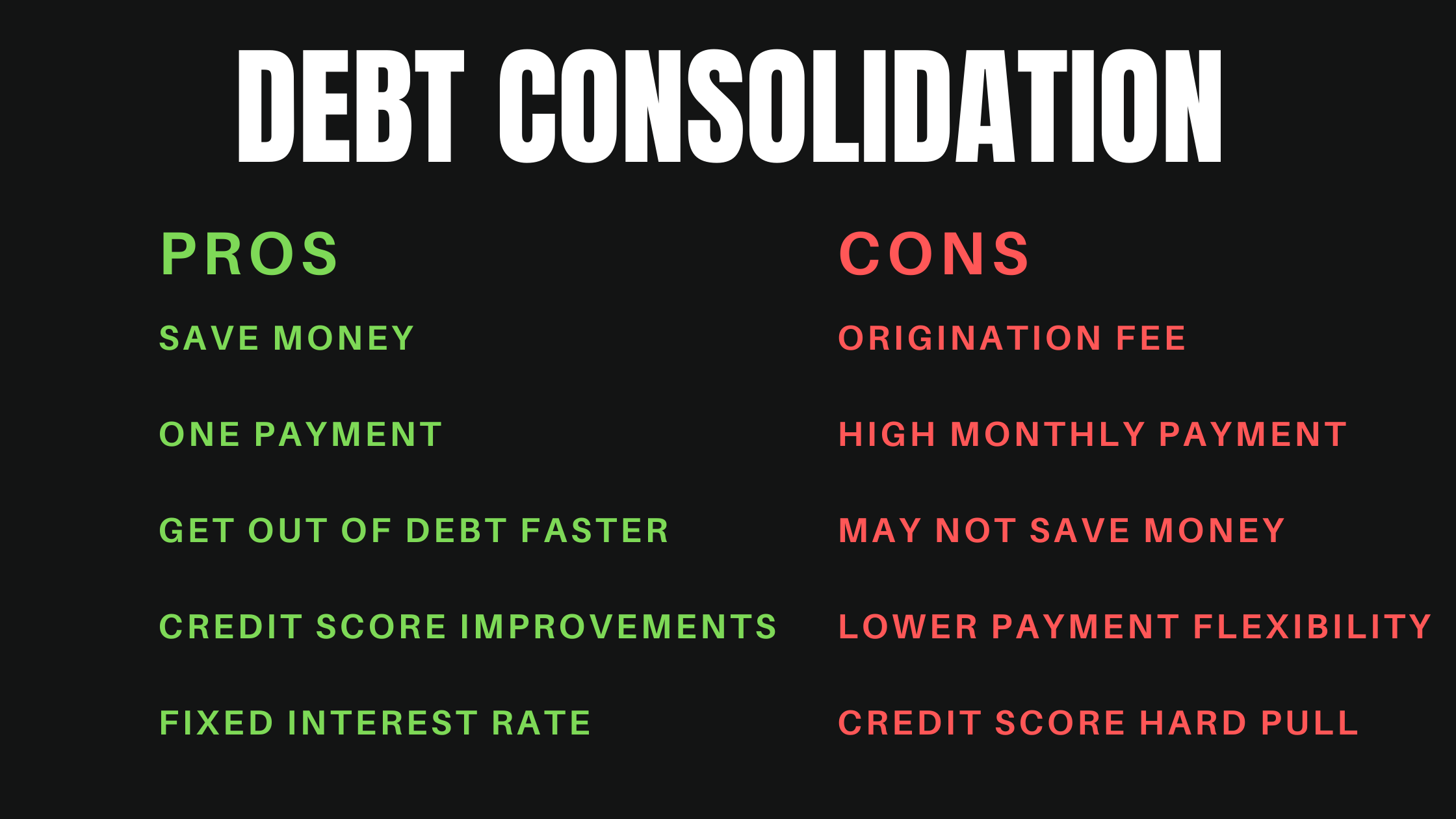

Quick summary: Pros and Cons of Debt Consolidation

| Pros of Debt Consolidation | Cons of Debt Consolidation |

|---|---|

| You can receive a lower rate and save money | You will have to pay an origination fee |

| You have one payment instead of multiple payments | Your monthly payment can be high |

| You can get out of debt faster | You may not save money on all of the debt you consolidate |

| Your credit score may improve | You may not have addressed the root cause of the debt |

| You will have a fixed interest rate instead of a variable interest rate | You may face lower payment flexibility if you face financial hardship |

| Your credit report will have a new hard credit pull |

Pros of Debt Consolidation

You can receive a lower rate and save money

One of the biggest draws of a debt consolidation loan is that you can receive a lower interest rate than your credit cards, saving you money in the process.

Let’s look at an example:

- Credit Card 1 = 27.99% interest rate, Balance = $5,000

- Credit Card 2 = 20.99% interest rate, Balance = $10,000

- Credit Card 2 = 14.99% interest rate, Balance = $5,000

In this example, let’s say you qualify for a debt consolidation loan of $20,000 at an interest rate of 12.99%.

Instead of paying higher interest rates on all of your credit cards, you will have just one payment each month at an interest rate that will save you money.

You have one payment instead of multiple payments

In the above example, we are looking at 3 credit cards that are consolidated into 1 debt consolidation loan payment. With debt consolidation, the more payments you are consolidating can simplify your life drastically.

Let’s look at the following example where a debt consolidation loan may be more appealing.

- Credit Card 1 = 27.99% interest rate, Balance = $5,000

- Credit Card 2 = 20.99% interest rate, Balance = $10,000

- Credit Card 2 = 14.99% interest rate, Balance = $5,000

- Debt consolidation loan 1 = 19.99% interest rate, Balance $3,000

- Medical bill 1 = Balance = $4,500

- Medical bill 2 = Balance = $700

- Payday Loan = 200% interest rate, Balance = $1100

- Car Loan = 19% interest rate, Balance = $8,000

As you can see, with a debt consolidation loan of around $38,000, you would consolidate 8 monthly payments into just 1 monthly payment.

So, a debt consolidation loan can simplify your life through fewer monthly payments.

You can get out of debt faster

Paying the minimum payment on your credit cards each month means that it can take years to payoff your balance. Many people make just minimum monthly payments, and according to one study, only 1% of credit card accounts adopted the suggested payoff plans offered by credit cards to get out of debt in 3 years instead of many more years.

Thankfully, a debt consolidation loan is often on a 3-5 year fixed payment plan, so you now get the accountability to payoff your debt faster than if you would make minimum payments.

Your credit score may improve

Your credit mix accounts for 10% of your credit score, which is the diversity of the types of credit in your portfolio (loans, credit cards, mortgages, etc.). So, a debt consolidation loan can help your credit score.

Also, when you pay off all of the balances from your debt consolidation loan, that shows positive behavior.

And, as you pay off the balances faster, you’re over-credit utilization will decrease, leading to a potentially positive credit outcome.

You will get out of debt in a fixed amount of time

One of the biggest advantages of a debt consolidation loan is that it is an installment credit instead of a revolving credit. This essentially means that there is a fixed period of time when your debt will be completely paid off.

As stated above, you could make a credit card minimum payment that takes over 10+ years to get out of debt, and a personal loan that doesn’t allow new credit to be added can be 3-5 years.

The above scenario is assuming you do not take out additional debt on the credit cards that you consolidated, and we will cover that in the cons section later.

You will have a fixed interest rate instead of a variable interest rate

Debt consolidation has a fixed interest rate at the time when you take out the loans. With the interest rates increasing in 2022, you could see many banks issuing credit cards following suit by increasing the variable interest rates on credit cards. With credit cards, your credit issuer is not even required to provide a 45-day warning of the increase.

So, a debt consolidation loan can be extremely helpful because you lock in the interest rate when the loan originates, similar to a mortgage loan.

Cons of Debt Consolidation

As someone who worked in debt consolidation, I believe I have a detailed understanding of the cons of debt consolidation that many people may be unaware of.

You will have to pay an origination fee

A loan origination fee can range between 1 and 8% of the origination amount. The fee is basically the cost of the loan provider to originate the loan. This can include the costs of doing underwriting, pulling credit reports, etc. The fee may depend on what type of loan you are taking. For example, a mortgage origination fee can have an origination fee between 0.5 and 1%, and a debt consolidation loan origination fee can be between 4 and 6%.

While the fee is often necessary, it’s important that you understand that it can be a high cost and is also removed from your loan amount.

For example, let’s say you took a debt consolidation loan of $10,000 with an origination fee of 5%. You would get $9,500 in your bank account, but pay off the loan as if the balance was $10,000.

Please be sure to review the truth in lending disclosure to confirm how the origination fee is taken from your loan. For example, I have heard of lenders that may add the origination fee on top of the loan amount, which may not be in your best interests.

Your monthly payment can be high

One of the challenges is that the debt consolidation monthly payment may be more expensive than your minimum monthly payments.

Let’s say you have a total of $50,000 in credit card debt and are paying 1% each month for a total of $500. Your monthly payment on a $50,000 36-month loan could be well over $1,500 per month, which is $1,000 more than what you were paying off on your credit cards.

You may not save money on all of the debt you consolidate

This disadvantage is one of the least understood cons of debt consolidation. Let’s say you have debt that has a mix of interest rates, so a debt consolidation loan may not save you money on all of your debts.

Let’s take a look at the following example.

- Credit Card 1 = 29.99% interest rate, Balance = $5,000

- Credit Card 2 = 22.99% interest rate, Balance = $10,000

- Credit Card 3 = 18.99% interest rate, Balance = $5,000

- Credit Card 4 = 12.99% interest rate, Balance = $10,000

- Credit Card 5 = 7.99% interest rate, Balance = $10,000

- Credit Card 6 = 0% introductory interest rate, Balance = $5,000

Let’s say you qualify for a debt consolidation loan for $45,000 at an interest rate of 13.99% with an origination fee of 5%.

Unfortunately, you may not save money on all of the debt if you take this option because the 13.99% interest rate is higher than the credit card with a 7.99% interest rate. You would also need to consider the origination fee will decrease some of your savings.

You may not have addressed the root cause of the debt

A debt consolidation loan can save you money, get you on a fixed payment plan, and get you out of debt faster, but it may not solve the original root cause of debt if you got into debt because of spending habits.

For example, I have seen time and time again when an individual takes out a debt consolidation loan but doesn’t pay off all of the debt and then continues to accumulate debt on credit cards, leading the individual to financial hardship and potentially bankruptcy.

That being said, many people accumulate debt for unforeseen circumstances such as job loss or medical challenges, so spending behavior is not a problem.

You may face lower payment flexibility if you face financial hardship

When many individuals take out a debt consolidation loan, they do not consider they will face financial hardship. If a financial hardship such as a job loss or divorce happens, a loan provider may be less flexible than a credit card issue as a debt consolidation loan is fixed installment credit. Thus, it can be more difficult to extend the life of a loan. As such, many credit counseling agencies will not take personal loans when helping individuals.

Your credit report will have a new hard credit pull

While your credit score could ultimately improve, your credit score could decrease in the first month due to the creditor pulling a hard credit check. A hard credit check is one of the factors that contribute to your credit score and is seen by other lenders whereas a soft credit check is not.

While this is not a major con, it is an important factor to know when considering a debt consolidation loan as many lenders pitch that your credit score will not be affected when checking your rate. That said, your credit score may be negatively affected when you accept the rate presented.

If you for whatever reason accept the loan and then do not end up taking the loan, your credit score may keep the negative effects of that hard credit pull.

Let’s Summarize

A debt consolidation loan can provide an avenue to get out of debt faster and save money in the process. That said, you have to consider that you’ll pay an origination fee, your monthly payment may be higher than your credit card minimum payments, and you may not have addressed the root cause of the debt.

When deciding whether to get a debt consolidation loan, hopefully, this list of pros and cons of debt consolidation can help you make the most informed decision. Please comment if you have any questions or anything. Thanks!